Getting The Home Mortgage Closing Procedure To Work

The Best Guide To Steps In Closing A Home Loan

transfers ownership of your new home from the seller to you. Yes, there's a great deal going on, and also a whole lot of money is mosting likely to change hands. However when you recognize what to anticipate as well as prepare well, it can be a smooth, relatively low-stress experience.

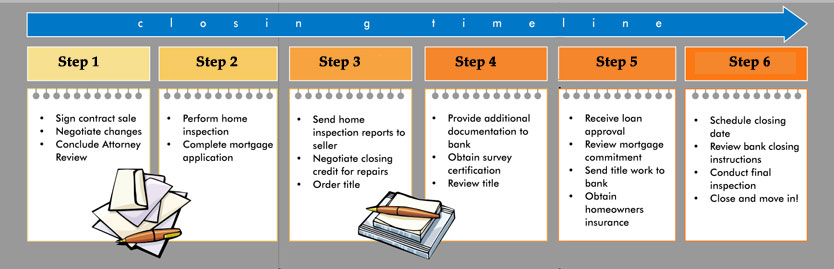

The home shutting process really starts as quickly as you and the seller have authorized an acquisition contract. Individuals commonly describe this duration as being "in escrow." What's the timeline? Generally four to six weeks. In limited markets, nevertheless, it can be as long as two months, due to the fact that it's harder for vendors to work with the sale of their home with purchasing another.

Closing on a house is a large offer, yet it could in fact be simpler than locating one that you desire and can pay for in the very first place. As well as when it mores than, you entrust to the tricks! And also a home loan. To seal the deal on your home, you need a closing agent (likewise called a negotiation or escrow representative).

In a lot of states, the closing representative is a neutral 3rd party who helps a negotiation business (usually called an escrow business or title firm). In some cases you can choose the company; this is frequently bargained with the seller. The standardized Finance Estimate form you received after you requested your finance notes the closing services you can buy (see page 2, section C).

The Buzz on Home Mortgage Closing Process

Yet others need one to prepare only specific files, so you end up with both a negotiation business and also a property lawyer. Which states require an attorney for all or part of the process? We think twice to offer you a listing, because regulations transform all the time. Most of them are eastern of the Mississippi.

Where an attorney is optional, you could desire one anyhow. Unless justpaste.it/6slut you hire your very own attorney, there's nobody at the closing who specifically represents your legal interests. If there's anything uncommon about the sale, certainly play it risk-free as well as work with one. Even the most effective property agent is not a property attorney.

Your state bar association may have a lookup. Per hour costs generally run from $150 to $350. Lenders need you to get home owners insurance policy and also bring the plan to the closing. That coverage is pretty crucial to both you as well as them! As you can envision, the price of insurance coverage differs widely depending on the value of your home, exactly how beneficial your things is, and also where you live.

Prior to you go shopping, take an appearance at these eight usual false impressions about house owners insurance policy. When you buy a home, you're buying the "title" to the home, which provides you single, clear possession. Title insurance provides security in the unlikely but potentially devasting occasion that someone else, someday, makes a surprise case on the residential property.

The smart Trick of Shutting A Mortage That Nobody is Talking About

The key point to understand is that you need your very own plan. Your lending institution will need you to buy title insurance policy to secure their investment, however their policy doesn't cover you. Technically, it's optional for you, but please don't pass on it. Without it, you can shed your house as well as your whole financial investment if your title ever were tested.

The price of a title insurance policy varies widely around the country. The standard is regarding $1,000. You can conserve money by buying both plans from the same company. Normally, the lender has a recommended insurance provider, but you have the right to pick a various one. Prior to you can close, you have to fulfill all the conditions established by your lending institution.

Some conditions could be specific to your finance, however typical ones consist of a clear title report, an evaluation number that goes to the very least the amount of the financing, documentation of your income, and also proof of insurance coverage. If you become worried regarding meeting any of the conditions, call your car loan officer ASAP.

Do yourself a favor and also start your arranging, packing, and also various other jobs early. You'll have enough on your mind on closing day without stressing over finding even more boxes. Below's a sanity-saving eight-week checklist for you. This essential record, a country wide standard form, makes a list of the closing sets you back to both you as well as the vendor as well as lays out crucial info concerning your car loan.

The Basic Principles Of Shutting A Mortage

The costs received the Closing Disclosure must be similar to what you saw on the Financing Price quote back when you got the funding. Any shocks? Start asking inquiries. The walk-through is a quick final check out your future house. Your representative will schedule it, ideally for the very same day you close.

https://www.youtube.com/embed/0pFnaj-B6iw

The walk-through might be quick, yet it isn't simply a rule. Prior to you take possession of the home, you need to see to it the seller actually has left as well as left points in the problem you concurred to. Every agent has stories: vendors that have not even started packaging, a smashed image window ... If anything is amiss, your representative will obtain on the phone promptly.

If the vendor was supposed to do anything major, have the work inspected by a specialist prior to the walk-through. The closing representative (whether that's a settlement business or your lawyer) will certainly send you a listing of everything you require to offer the closing. If you have any concerns, don't hesitate to call the closing agent or your loan provider.

The home loan and also other files are authorized, settlements are exchanged, as well as finally, the waiting mores than: you get the secrets. If you have any kind of unanswered concerns, this is your last opportunity. You'll be facing a rather big heap of paperwork. It's not so negative if you understand what's coming, so right here's a brief guide to your closing documents.

The smart Trick of Shutting A Mortage That Nobody is Discussing

If your closing agent is your very own lawyer, it will most likely go to their office. That will be there? This varies depending upon where you live. Your property agent can tell you what to expect. Sometimes there's an actual crowd, including the closing agent from the settlement firm, your attorney if you have one, the seller's attorney if they have one, the lending institution's representative, the seller, and both realty representatives.

You may have the keys, but you're refrained from doing yet. After you close, it's wise to file a homestead affirmation, also called a homestead exemption. In some states, homestead is automated, however don't think. Ask your property representative or closing agent concerning it. A homestead statement registers your residence with both the government and also state federal governments as your main home and also safeguards it in different means.

The details can be a bit complicated, but homestead usually obtains you at the very least 3 sort of defense: If you ever face bankruptcy, homestead can help avoid the forced sale of your home to pay debts, with the exception of the home loan (i.e. no help in a foreclosure circumstance), building and construction liens, and also real estate tax Exempts you from a particular quantity of real estate tax Aids a making it through spouse stay in the house To submit, call your county assessor's workplace.